The Path Becomes Credible Before the Destination Arrives

On the iPhone moment most observers are missing, the enablers that finally arrived, and why the next cycle will not look like the last one.

In June 2007, a device launched that did not invent the mobile internet but made it truly usable by a billion people for the first time. Within four years the structures of media, commerce, banking, and communication had all been quietly rewired. The companies that captured the shift were, for the most part, not the names that had dominated the previous dot-com wave. They were the ones quietly building through the bust, even as the visible activity was muted and most observers were drawing the obvious conclusion that the internet thesis had been overstated.

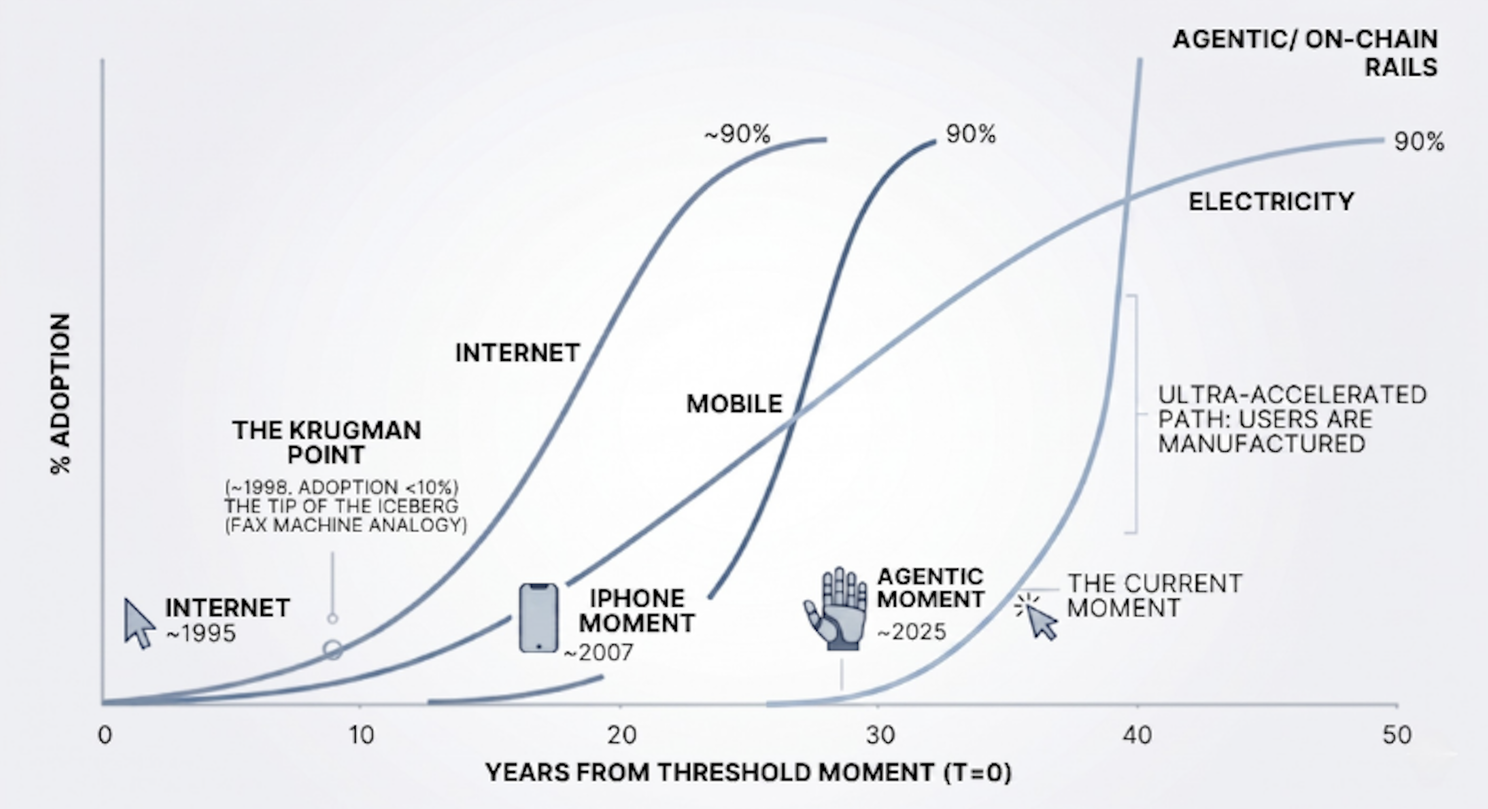

Not only do trends often build like icebergs with most of the mass hiding below the surface, each successive technology cycle also compresses faster than the one before it. Electricity took roughly half a century to reach most households. The internet took less than half of that, while mobile finally proliferated in under a decade. The cycle that is now unfolding will similarly move even faster, accelerating through the remainder of this decade.

The infrastructure for permissionless payment rails has been built quietly, largely hidden from view by what has been perceived as yet another technology slump. Once again, most observers are interpreting a lack of visible progress as evidence of failure. However, the iceberg is poised to reveal itself. What is different this time is the users, who do not need to be persuaded because they are being mass-manufactured, at a speed no previous adoption curve has ever had to absorb.

Those users are autonomous AI agents. Their arrival provides the missing link that will propel permissionless rails toward their 'June 2007' iPhone moment and abruptly end the prolonged stagnation of the crypto market. With the architecture finally complete and adoption igniting, those looking only at the visible activity will miss the move and head straight for a classic Titanic moment.

The Visible Activity, As Always, Tells the Wrong Story

The skepticism is not lazy. The visible numbers invite it.

Roughly four-fifths of the volume on x402, the most-cited agentic payment protocol, has been linked to wash trading, according to recent work by Artemis Analytics. Similarly, an analysis by Visa and Allium finds that less than a tenth of stablecoin volume is organic. By Juniper Research's count, total agentic commerce currently sits at a mere $8 billion globally, stacking up poorly against headlines that forecast trillions. Reasonable people have reached dismissive conclusions before, looking at numbers that turned out to be only the tip of the iceberg, and were later proven spectacularly wrong.

Krugman's Mistake

In 1998, Paul Krugman wrote that "by 2005 or so, it will become clear that the Internet's impact on the economy has been no greater than the fax machine's." A Nobel laureate in economics, looking carefully at the visible activity of the day, concluded in print that the internet was a fad whose significance was already overstated.

Krugman was not stupid. He was reasoning correctly from incomplete information. The internet did not turn out to be a faster fax; it was a structural collapse in the cost of moving information. That single shift birthed an entire generation of novel business models that were invisible and, often, practically infeasible from the vantage point of 1995.

Software delivered as a service rather than as a product. E-commerce as a category. The platform economy. Search reimagined as a business in itself. The shift of most consumer commerce, most media, most communication, from physical channels to digital ones. A shop in a small town now selling globally, without the storefront, without the inventory, without the staff.

The shift from bricks and mortar to bits and bytes was simply not visible from where Krugman was standing. Our lesson today is not that he was uniquely wrong. It is that those who are merely observing the visible activity in the current cycle are at risk of making the same kind of mistake.

The Forecasts That Did Not Land

For all its success in rewiring the world, the internet also did not deliver everything that was expected. Important overlooked opportunities have stalled, pending the arrival of the rails required to make them viable.

A decade ago, the sharing economy was forecasted to be measured in trillions of dollars by now. Spare rooms, spare cars, spare tools, all monetized through internet-native marketplaces matching strangers at scale. McKinsey, PwC, the World Economic Forum, among others, all laid out their trillion-dollar projections.

Yet, only Uber and Airbnb worked, almost nothing else scaled.

The reason was neither technical nor regulatory. While the internet reduced the cost of moving information, it did not reduce the cost of trusting the stranger at the other end of the transaction. This is important as a meaningful share of global economic activity is consumed by exactly the issue that strangers cannot trust each other directly. Auditing, verification, reconciliation, compliance, intermediation, dispute resolution, the whole apparatus that economists working in the transaction-cost tradition have long estimated runs, in aggregate, on the order of a tenth of GDP.

Sharing your apartment, your car, your tools, or your time with someone you have never met imposes the whole trust overhead directly at the level of each individual transaction. Verification, dispute resolution, insurance, reputation systems, and intermediary platforms often take up to a 30% cut to hold the arrangement together. That cost crushed the economics of every category beyond the very few that could brute-force scale.

McKinsey recognized this. In its 2018 work on blockchain's strategic business value, the firm made the explicit case that distributed-ledger infrastructure could systematically reduce the cost of trust and thereby unlock entire categories of business model that were previously economically unviable in a world where that same trust had to be manually brokered and couldn't be encoded.

That call did not pan out. Now, eight years later, the trust layer still looks identical to how it looked in 2017. By today's visible data, McKinsey's call has not panned out.

Hold that thought. We are coming back to it.

Pets.com Was Not Evidence of a Fad

In 1999, Pets.com raised hundreds of millions of dollars on a real business model. Sounds perfectly reasonable; an online retailer for pet food and supplies, going after a category with predictable demand and high purchase frequency. However, a year later, by November 2000, it was bankrupt.

The business model was not wrong; it was just prematurely launched. The supporting infrastructure for online retail at consumer scale, including cheap last-mile logistics, mobile commerce, and digital payments that worked, was not yet in place. It was, in a nutshell, the cost of shipping a bag of dog food that obliterated the unit economics, while the rest of the necessary enablers also would not arrive for yet another five to ten years.

Pets.com was essentially a stereotypical casualty of the dot-com bust, but the downturn itself was not evidence that the internet was a fad. It was instead evidence that the enablers were not there yet. By 2005, as the dot-com bubble was five years in the rear-view mirror, the survivors of the carnage had already quietly assembled most of the foundations of what would become the real wave.

Most observers were still reading the visible muted activity and concluding that the original thesis had been overhyped. However, they were fixating on the tip of the iceberg and missing the mass gathering momentum beneath the surface; when a weight of that magnitude finally shifts, it does not create a wave. It generates a tsunami.

The crypto cycle from 2017 to 2021 had the same anatomy.

Vast capital was raised on the McKinsey trust thesis and on the promise that blockchain would systematically reduce the cost of coordination between parties who could not trust each other directly. Almost none of it was realized.

Strip out the ten biggest crypto tokens and the picture is unmistakably clear. The long-tail altcoin index (OTHERS) went from a highest daily close of $68 billion at the start of 2018 to $437 billion at the November 2021 peak, and has never since broken those all-time highs. The long-tail crypto bull market never properly returned; consequently, the current state of the market, five years on, looks dismal by the standards of the 2021 heydays.

Exactly like the aftermath of the dot-com bubble, this once again feels like evidence of a broken thesis. However, just like back then, that conclusion is wrong. It is simply evidence that the enablers for unleashing the promise of trustless blockchain rails were not yet there.

Blockchain Failed With Humans

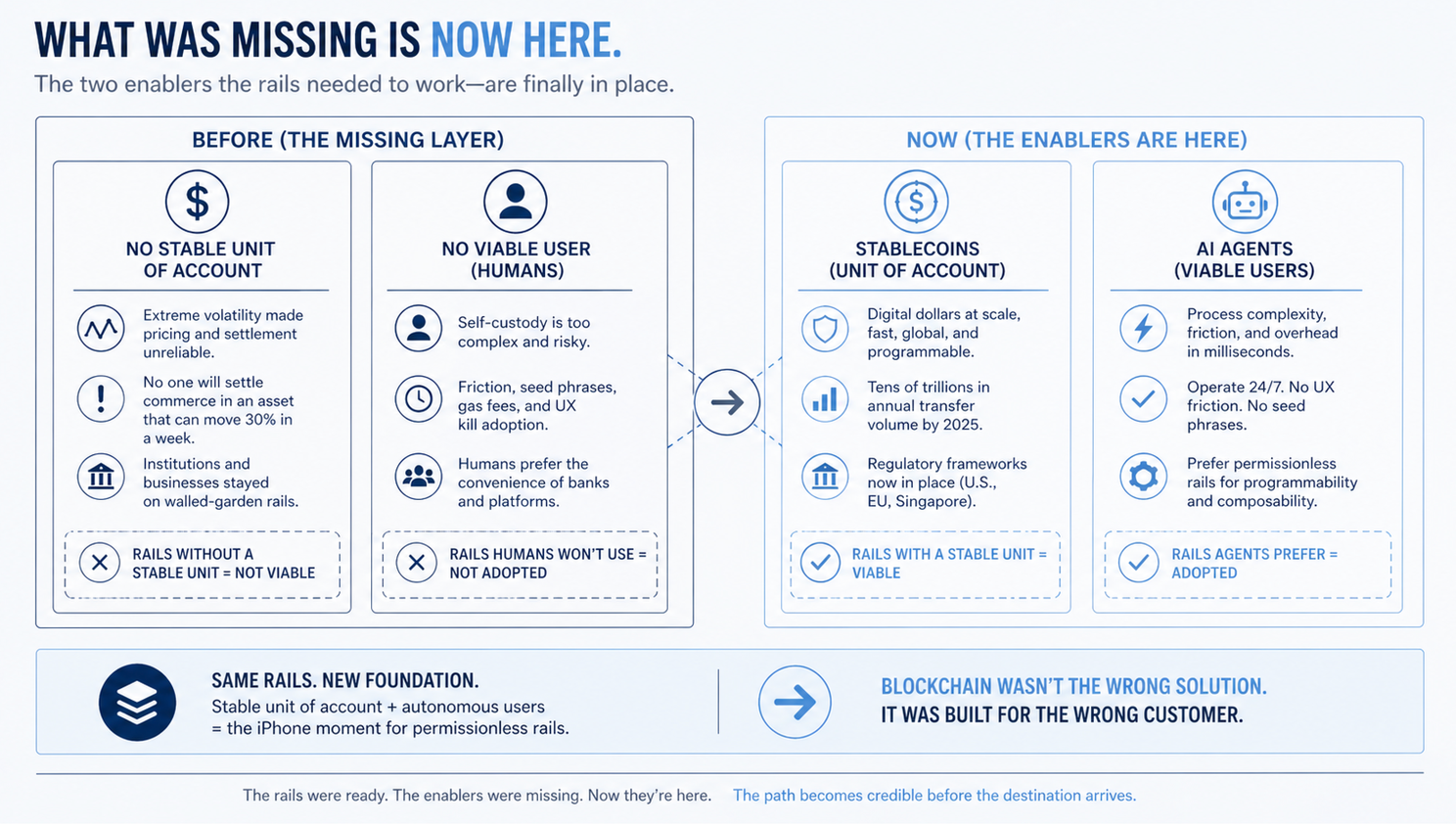

Two things had to be true for the McKinsey trust thesis to deliver. Firstly, the rails needed a stable unit of account, because no one was going to settle commerce in a currency that sometimes moves 30% in a week. Secondly, the rails needed a willing and able user, because the friction of permissionless infrastructure is real, and the average human consumer was never going to give up the convenience of a bank for the burden of self-custody, with their entire balance hanging on a seed phrase.

The first problem was solved by the most boring of all crypto applications: stablecoins. They gave the permissionless rails a unit of account that is, in the end, just good old boring dollars. By 2025, they were carrying tens of trillions in annual transfer volume, supported by the arrival of clear regulatory frameworks in the United States, Singapore, and the European Union. A stable unit of account is no longer an unresolved issue.

The second problem is being solved by a fundamental inversion most observers have not yet registered. Blockchain was not built for the wrong purpose; it was built for the wrong customer.

The right customer is not a human. It is an autonomous AI agent.

Agents do not mind any of the friction that stopped humans. The long wallet address, the multi-step authentication, the cryptographic signature, the gas fee. The procedural overhead that blocks a human treasurer at a midsize company is what an agent processes in milliseconds without complaint. Agents, in fact, prefer permissionless rails, because programmable settlement and conditional release give them properties that account-to-account systems and card networks structurally cannot offer.

For years, observers have said that crypto was searching for a problem to solve. They had it backwards. The problem was real. What was missing were the enablers. Stablecoins gave the rails their unit of account. Agents are now giving them their user. This convergence is the equivalent of the iPhone moment for permissionless rails, in the precise structural sense that matters. The LLM is the device. The rails are the network. Each was largely useless without the other, and together they constitute the substrate for a new kind of commerce.

Which brings the obvious question back into view. Why should anyone trust McKinsey's new forecast, the one that puts orchestrated agentic commerce at $3 to $5 trillion globally by 2030, when their last call on this same underlying thesis did not land for eight years?

The answer is that this is not a new forecast. It is the same forecast. The trust thesis from 2018 is the agentic-commerce thesis from 2026. The earlier call did not pan out because the enablers were missing, and the later call will pay off now that the enablers are arriving. McKinsey could even be conservative this time, because they are still forecasting based on business models that already exist as categories, rather than envisioning new emerging ones that nobody has yet been able to conceive.

Markets for spare compute capacity sold in inference cycles. Energy traded between rooftop solar arrays and electric vehicles at the edge of the grid. Verified data exchanged between agents at machine velocity, with payment released on cryptographic proof of delivery. Machine-to-machine SLAs settled on telemetry without human arbitration. None of these existed as categories in 2018, because none of them were possible.

The Sharing Economy, Finally

The sharing economy did not yet deliver as McKinsey and everyone else expected. It may now finally deliver, with agents handling the coordination on trustless crypto rails that no human-scale platform could economically carry.

The reason it did not scale beyond Uber and Airbnb was that the cost of trust consumed the economics of every category beyond ride-hailing and short-term rentals, where the unit economics were strong enough to subsidize a heavy intermediary layer.

Once trust is embedded directly at the protocol level rather than by a platform levying up to a 30% margin, and once the coordination between strangers is done by agents at machine velocity rather than by humans paying attention, the categories that were previously economically unviable inevitably become feasible.

Peer-to-peer rental fleets where households put cars, power tools, lawnmowers, and other durable household goods into continuous market circulation. Hyper-local labor markets where micro-services route seamlessly between strangers. Direct food and hospitality networks and so much more that was imagined already a decade ago but never took off as the unit economics failed to support the required trust layer.

What is missing from this list are the parts nobody can yet name. After the dot-com bust, nobody envisioned social media as the dominant attention economy, streaming as the default media model, the smartphone as the universal computing layer, or the SaaS, cloud, and API economy as the substrate of modern software.

These were invented in the years after the wreckage by people who looked at what the survivors were quietly building and saw what the rails could now carry. The same will be true of the next five to ten years as agentic AI and blockchain converge.

None of this happens, neither the sharing economy renaissance nor the expansion beyond it, without resolving how regulation binds an autonomous agent to an accountable entity. The identity frameworks of the traditional financial system were not designed for autonomous agents acting on behalf of a principal, and bridging that gap is the real infrastructure challenge of the next phase.

The Path Is Already Being Priced

Uber was founded in 2009. It went public in May 2019 at an $82 billion valuation. It posted its first annual profit in 2023, fourteen years from founding to profitability and four years from IPO to profitability. By the time the company became profitable, however, it was already worth between $150 and $200 billion.

The market was not pricing the profit. It was pricing the credibility of the path.

This is what valuations do when a transformative thesis starts becoming credible. They run ahead of the destination, sometimes by years, sometimes by decades.

Amazon was worth roughly $30 billion in late 1999, at the peak of the dot-com bubble. Within two years it had crashed by 90% to under $3 billion. The path, nevertheless, remained clear; it was simply pending the arrival of the enablers required to make it viable. In 2006, as ubiquitous broadband finally provided high-speed connectivity, Amazon launched AWS. This was the cloud computing infrastructure that would go on to redefine the internet and trigger a structural repricing that eventually sent the company's valuation into the trillions.

The destination glimpsed in 1999 took years to arrive, but once the broadband-enabler was in place, the trajectory became unstoppable. Blockchain is approaching its AWS moment now, as agentic payments and AI governance are about to move on-chain. The current state of the market is consistent with a market that glimpsed a trillion-dollar future in 2021, but has not yet priced the path because the enablers were missing.

The 2021 peak was a muted version of 2017. The next repricing, when it comes, will not look like 2021. It will look like 2017, or it might even be more violent, because the underlying thesis is finally deliverable, and the window for a real and sustainable repricing of serious crypto infrastructure is opening.

What This Means

Only the tip of the iceberg is visible now, but as we have seen, one can look beneath the surface to measure the mass.

The skepticism about agentic payments is well-founded as far as the visible numbers go, in exactly the same way the skepticism about the internet was well-founded in 1998, when the visible numbers were modest and Paul Krugman equated its future impact to that of the fax machine.

The forecasts that did not pan out, from McKinsey's trust thesis to the trillion-dollar sharing economy and the capital-heavy crypto cycles that stalled, were not wrong. They were just early as the enablers were missing.

Stablecoins are now providing the rails with a unit of account, and agents are turning out to be the users the rails were built for. The crypto slump is the dot-com bust analog and it is now five years behind us. As technology cycles continue to compress, the present moment sits at the equivalent threshold of the iPhone launch, the catalyst that unshackled the internet from the desktop just as agents will liberate blockchain rails from human friction.

The path is becoming highly credible, although the destination still remains years away. However, as we have seen, markets do not wait for the destination. They move when the path becomes credible, and they move most violently once previously dismissed infrastructure suddenly finds the user it was built for and adoption accelerates.

That is the part most observers are still reading wrong. They are looking at the empty lanes and calling the road a failure, unaware the final bridge has just been laid. By the time the traffic is undeniable, the path will already be priced.